They have been called many things – mercenaries, irregular forces, private military contractors (PMC), and private security companies (PSC) – whatever the phrase, PMCs have been around for a very long time.

The war in Ukraine recently brought the use of private soldiers into focus – Russia has hired at least three such groups, the Wagner Group, Redut, and Patriot Private Military Company, to fight in Ukraine.

PMCs are a growing international business.

There are private military contractors from all over the world, including the US, Russia, Iran, Canada, and South African. Many are former elite military combatants, more skilled than local forces. The biggest contractor of PMCs is the US government but that may have changed with the Ukraine war.

PMCs in history

The most well-known example of PMCs in the world was the military group who worked for a woman pirate named 石陽, Queen Shí Yáng, also known as 鄭嫂. Queen Shí Yáng had 70,000 men who worked for her aboard more than 1,600 vessels. In the early 1880s, they controlled the South China Sea and Pearl River Delta, routinely defeating the Qing Dynasty navy in coastal battles.

Shí Yáng’s group earned revenues in a variety of ways, including as mercenaries for warring Vietnamese rulers, by controlling the importation of salt into China, by collecting navigation taxes, and looting foreign vessels entering China’s waters. Mercenaries were paid 20% of all the loot collected by Shí Yáng.

The Roman Empire had PMCs called the Praetorian Guard. They were private soldiers who, for over 300 years, protected powerful generals and politicians. Wealthy families often had thousands of praetorians safeguarding their family, land and business affairs. Praetorians became a powerful group in Rome, and the more powerful among them, at one time came to control who would succeed as emperor of Rome.

YouTube channel of Invicta

Medieval Europe had a booming conflicts market, and PMC were used to engage in wars, steal land or to protect businesses for the wealthy.

Byzantine emperors hired Norse PMCs known as the Varangian Guard. In the 11th Century, nearly half of William the Conqueror’s army was made up of PMCs, and King Henry II hired PMCs to deal with the rebellions of 1171–1174. The Pope’s Swiss guards, now part of the Swiss Army, used to be PMCs.

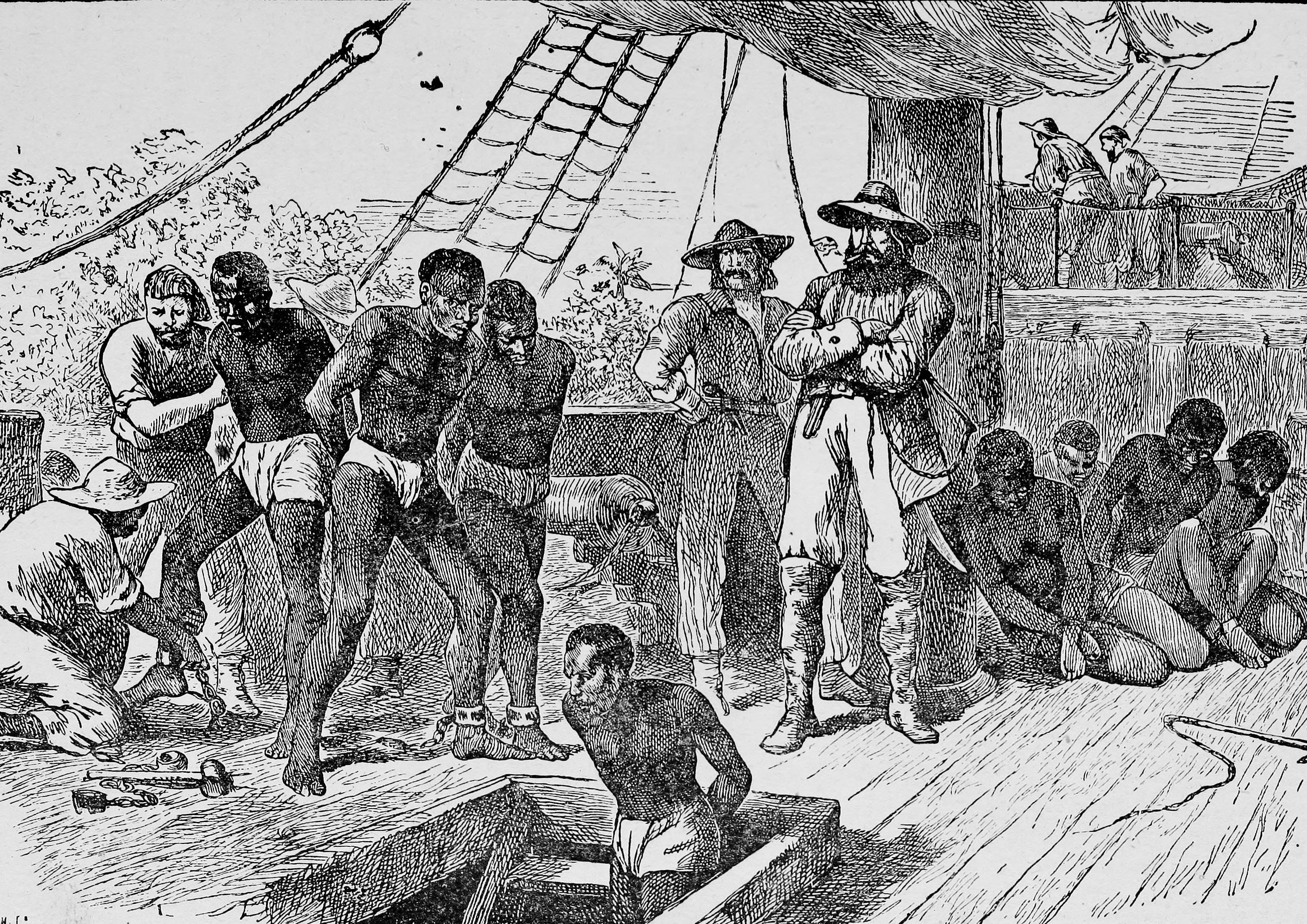

An obvious example of the use of PMCs, but the least discussed, was the use of PMCs in the enslavement trade. Henry Bath, in his book series “Travels and Discoveries of North and Central Africa”, which describes his mission to several countries in Central Africa in 1856, details the use of local armed private forces hired by foreigners to capture humans in Central Africa for enslavement.

Illustration of Enslavement (Source: John William Frost’s book Broken Shackles)

PMCs, in one form or another, have always been part of the culture in manufactured and real conflict zones, hired to protect legal and illegal commerce for private enterprise, organized crime and in some cases, for governments.

The Wagner Group is owned by Russian oligarch Yevgeny Prigozhin. Prigozhin became acquainted with Putin when Putin was a municipal politician in St. Petersburg. Murdered Russian organized crime leader Shabtai Kalmanovich, was part of the same circle in St. Petersburg. Before Kalmanovich was horse-traded back to Russia from an Israeli jail, he used PMCs to engage in diamond and minerals trafficking in Sierra Leone, and to protect Joseph Momoh.

Defending extraction rights

PMCs continue to be frequently used to protect mineral resources for private enterprise, including in large part, by Canadian owned extraction industries.

Some PMCs act as intermediaries for black bag deliveries. Black bag deliveries (called black suitcases in Europe and Asia) are corruption / bribery payments made to politically exposed persons (often politicians), a common occurrence in the mining and extraction industries in Africa.

The Wagner Group is one of the PMCs operating in the Central African Republic on behalf of the government, and to protect private mining companies.

https://youtu.be/1tECHzB-uCM

PMCs remain the protectors of mining assets and mining rights in most conflict areas of the world because they are effective at what they do for private commerce. Many public and private enterprises could not operate in conflict zones without PMCs because the risks to assets, investments, manpower, infrastructure and executives are extremely high. PMCs mitigate risks.

The mining company Freeport-McMoRan hired the PMC company Triple Canopy to protect its mining rights and mining operations in Papua, Indonesia, against local insurgents. In South Sudan, DeWe Security provides PMC services to protect the contractual rights and operations of the China National Petroleum Corporation.

PMCs also operate in Syria, to protect oil and gas assets, and in Mali, under contract with the government.

YouTube channel of VOA Africa

PMCs can be effective

PMCs can be effective.

PMCs from South Africa and Eastern Europe were hired by Nigeria for a search and destroy mission to eliminate the terrorist group Boko Harem from Nigeria. They drove out Boko Haram in weeks – something the Nigerian military had not been able to do in six years.

Another PMC group, Executive Outcomes, was paid US$1.2 million a month to successfully contain and quell a rebellion in Sierra Leone. In comparison, the United Nations went through US$47 million for one month in Sierra Leone with zero impact.

In Somalia, PMCs hired by the UAE and the Somalian government effectively eliminated the piracy problem in the waters off the coast of Somalia. According to Lloyd’s of London, there have been no attacks on merchant vessels off Somalia for the last four years, saving US$6 billion in costs.

In the 2011 clip below, PMCs from the Trident Group, open fire on Somali pirates and prevent a pirate attack.

YouTube channel of Inbound Logistics

PMCs used to obstruct justice

PMCs also provide intelligence and pre-litigation services.

In Canada, the Israeli groups Tamara Global and Black Cube, run by former Mossad agents, were used in a litigation connected to Ontario lawyers, to come to Canada to obstruct justice and defeat the rule of law in a civil proceeding.

The mission?

To locate an Ontario Supreme Court judge named Frank Newbould, who presided over a key litigation, and once located, to lie to Newbould so that he agreed to a meeting. And at the meeting to engage him in a conversation under false pretenses, to egg him on to make anti-semitic statements, which would then be used as grounds for appealing a court decision.

The mission was successful except for the last part because Newbould did not make anti-semitic statements at the meeting.

The use of foreign PMCs in the obstruction of justice in Canada is probably less shocking than the fact that nothing happened to the lawyers involved in the plot.

Dangers of PMCs

The use of PMCs is growing throughout the world and there are dangers associated with their growth, beyond manipulating courts and interfering with the administration of justice.

The attractiveness of PMCs to those who hire them is that they provide deniability, which means they act in a foreign country in a vacuum outside the rule of law.

Among the dangers is that the super rich, the fortune 500 executives, will be able to buy power, leading to a situation where, with private armies, they become more powerful than some countries. The super-rich will become superpowers, and above the law.

Another danger is that while PMCs are stateless (meaning the men and women who sign on to be PMCs can come from any country), locals see them as a representative of a country. Blackwater, for example, was seen by the Iraqis and Iranians are being the US military, as opposed to simply PMCs. The Wagner Group has more than just Russian nationals engaged to perform PMC work, but locals in African countries, and in Syria tend to see them as tantamount to the Russian military.

For example, a PMC group comprised of contractors from France in Serbia will be viewed by Serbians as if they are an arm of the French government, even though they are a private group whose paymaster may be a private sector company. Any unlawful, menacing or inappropriate conduct will be attributed to the French government, which harms its international reputation.

There is also the danger that wars could be started without states. In the CAR, for example, and specifically, it is not beyond the realm of possibilities that another PMC group is hired to battle the Wagner Group and, among other things, to attempt to gain control of the mining infrastructure they protect for their clients, or to destabilize existing mining activities for another actor whom that PMC is fronting for.

This is a risk for many African countries that, hiring PMCs to support economic growth and protect foreign investment, may cause other non-transparent actors to use PMCs to engage in commerce-related warfare to gain competitive advantages illegally, especially those with viable deposits of rare earth elements and critical minerals.

Most countries use PMCs, and allow them to operate – tacitly or overtly. With armed non-state private military actors assuming more control in more areas around the world, state power will decline, which has the potential to upend international relations as we know it.

Another crypto company bit the dust early this week, and with it, up to US$10 billion in customer money evaporated. BlockFi was a digital currency exchange, deposit-taking institution, and lender. BlockFi also issued and sold securities. It was not government-registered to provide any of those financial services in Canada. In early 2022, it settled a case with the SEC for misrepresentations made to investors.

SBF

Like many others in crypto before it, it promised to “protect your assets” if consumers used its services. On Monday, it filed for bankruptcy protection. According to the bankruptcy filings, consumer assets were put at risk and not protected.

In the past few months, a slew of crypto companies – Terra-Luna, Three Arrows Capital, Celsius, Voyager Digital, FTX and now BlockFi – have gone kaput, and with them, billions upon billions of dollars of customer money are gone.

Voyager Digital is in a different category than the others because it is a Canadian public company, and one of its directors was a lawyer in British Columbia. It is being sued in the US for being an alleged Ponzi scheme.

The combined losses of those six crypto companies are of unprecedented proportions. This isn’t a Bernie Madoff sized evaporation of customer money held in trust – it’s many Madoffs. Before it blew up, CME Group CEO Terry Duffy said FTX was a pump and dump scheme, eg., like a capital markets fraud scheme.

Some of the founders of the six defunct crypto companies fled to extradition-friendly countries, where they are now professing their innocence in the court of Twitter.

It seems obvious that many crypto guys are not good at running companies but they seem exceptionally good at the art of deception.

Crypto dudes fool everyone

These crypto dudes fooled executives at the Ontario and Quebec pension funds, they fooled lawyers, they fooled banks, they fooled experienced venture capitalists, they fooled journalists, they fooled members of parliament in several countries, and they fooled regulators.

Canadian Kevin O’Leary talks about how he was fooled too, and talks about being targeted with hate on social media (and by the media) for his ties to FTX (here).(Footnote 1)

We got a taste of early deception in 2017, when a Canadian crypto dude settled with the SEC (see here) for lying in a pitch deck, on phone calls and in emails to banks, lawyers and investors about advisors, claiming untruthfully that several prominent people were advisors of his crypto company. Not only were they not advisors, but they had no knowledge that their likeness, bio and name were being used without consent to raise money, until reporters called them.

In crypto culture, some of these guys don’t just fib about advisors, high investment returns or the protection of customer assets – the US government warns that some are impersonating people (see here) as part of their business model.

Where were regulators?

The effects of the six crypto debacles, including British Columbia based Voyager Digital, are rippling across the globe, leaving many wondering how such vast schemes went on for so long without regulators stopping them, despite numerous red flags and warnings.

It’s not like there are no laws to protect the public from this. In Canada and the US, numerous laws, including securities, consumer protection, competition, banking, fraud, financial crime, and lending laws all have a role to play.

Round-tripping

One of the things emerging from these six crypto debacles is the extent to which crypto is a clubby, secretive world of guys who all know each other, and do transactions between each other. Not only that, if one looks at all of them together, it appears that some of them may have allegedly fronted for each other’s balance sheets or engaged in round-tripping.

Round-tripping is a type of activity where money (or crypto) is moved in a circuit. It’s a type of financial magic trick that creates the illusion of having funds (or of solvency, assets, or revenues). Round-tripping is unknown to most professionals except in the world of public auditing. We wrote about round-tripping in the capital markets here and here.

With multi-party round-tripping for credit, a number of companies send money to each other, one by one. When credit is obtained by party one, the money is sent to party two. When credit is obtained by party two, the money is sent to party three. Around and around, it goes. The result is that the amount of credit extended by victim banks or other parties balloons, filled with hot air.

Financial magic

Like all magic tricks, the illusion only lasts so long. The balloon must burst.

A user on Twitter questioned the money movements of BlockFi and FTX, which we’ve paraphrased:

“BlockFi gave hundreds of millions of dollars to FTX; FTX gave it to its Alameda branch; Alameda gave it to Emergent, a shell company owed by SBF, FTX’s founder; Emergent used the money to buy shares of Robinhood; the Robinhood shares were used as collateral for a loan from BlockFi to FTX; FTX then used that money to bail out BlockFi.”

Changpeng Zhao, the CEO of the world’s largest crypto exchange, Binance, also tweeted about the money movements. We’ve paraphrased what he wrote like this:

“Voyager Digital gave hundreds of millions to Three Arrows Capital; FTX-Alameda gave $100 million to Three Arrows Capital; FTX-Alameda gave $110 million to Voyager; FTX-Alameda then borrowed $377 million from Voyager; Three Arrows Capital went bust; Voyager went bust.”

And then FTX went bust. And then BlockFi went bust.

A circus

But its circuitous, right?

It was a kind of a merry-go-round of the same money spinning between many of these kaput crypto companies. Unfortunately, there were no adults in sight to turn off the circus lights at midnight and send the kids home.

1: In that interview, O’Leary pitches using Canadian digital currency exchanges, which he alleges are “safe” if they are public companies – we know that isn’t the case because of the Voyager Digital case – it was a Canadian public company that was a digital currency exchange. FTX operated in several provinces in Canada, as well, as a digital currency exchange and it was not “safe”.

The petrol mafia case was first police case of ‘Ndrangheta and Camorra convergence across Italy

A Deal with the Mafia

Anna Bettozzi with high boots, fur and a helicopter (Source: Instagram)

Here’s a question – what do you do to revive a failed oil business you inherited if you have no business skills and no money?

You might make friends with a Mafia associate on Facebook. And if you’re going to do this, you might as well go big and partner with the most feared and secretive Mafia organization in the world, the ‘Ndrangheta. If it goes bad, you might be dead; if it goes well, you might build a billion-dollar empire of dirty money.

That’s what Italian singer Ana Bettz did.

She almost couldn’t help herself – she was set to lose her luxury hotel apartment in the fashionable district of Milan, her Bentley and Rolls Royce, and access to plastic surgeons on speed dial.

Ana Bettz, who is really Anna Bettozzi, went to the powerful Camorra families in Naples and the dreaded ‘Ndrangheta in Calabria to finance her entry into the criminal world and become a petrol Mafia.

With their help, she built a billion-dollar empire that spread across Europe, using numerous shell companies to traffic in petrol and launder hundreds of millions for the Mafia.

A Ride to the Cannes Film Festival

It almost came crashing down in May 2019.

Bettozzi was on her way to the glamorous Cannes Film Festival in France to party with the rich and famous, being chauffeured in her favorite car – the Rolls Royce. Her deal with two of Italy’s most powerful Mafia groups was going well; business was booming.

The six hour drive from Milan to the Italian northern border town of Ventimiglia was pleasant enough; she could see Sardinia, her homeland, in the far distance across the glittering blue Ligurian Sea, as the car raced along the Italian coast.

In the trunk of the Rolls, she had stuffed €300,000 in dirty bills into a pair of high boots – a perfect way, she thought, to smuggle cash into France and avoid making a currency declaration at the border.

She had to hide the cash otherwise it would raise messy questions about its provenance.

She couldn’t exactly tell French border guards that it was from bootlegging oil with the ‘Ndrangheta. They would call Italy’s financial police, the Guardia di Finanza, and anti-Mafia investigators, the Direzione Investigativa Antimafia (DIA). The gig would be up and she couldn’t risk that. It wasn’t just the police she would have to face; she would also have to face the Mafia.

Under Surveillance

If Bettozzi had been paying attention during the trip from Milan to the French border, she might have noticed that the DIA and the Guardia di Finanza had been following her Rolls Royce for over six hours, from the moment she had stepped out of the lobby of the Gallia Hotel that morning.

The ‘Ndrangheta and secret service agents share a common operating rule – always have a mirror to your back. Bettozzi preferred her own rule – keep the mirror on your own face. For the past few months, teams of federal law enforcement agents had her under surveillance after she came on their radar when she made a call to the Mafia on a phone line they were intercepting, discussing the petrol smuggling business.

As the Rolls passed though the small town of Ventimiglia and approached the Italian-French border, the Guardia di Finanza made their move. They stopped her car before she could enter France. Bettozzi was detained.

Call to Mafia Lawyer

She asked to make a call to her lawyer – Ilario D’Apolito. She was playing right into their hands. You see, D’Apolito was the lawyer for the petrol trafficking operation with the Mafia who, police say, allegedly incorporated shell companies for the criminal operation.

He was one of the people they were investigating as part of “Operation PetrolMafias”. There were wiretaps on their phones, so police were listening when Bettozzi called her lawyer after she was detained. Whatever she said to him wasn’t privileged or confidential because that does not apply when lawyers are used (wittingly or not) for fraud or crime.

Bettozzi told the lawyer that she had been stopped and detained. She was panicking – not because of the €300,000 stuffed in her high boots – but because she had a safety deposit box key in her purse and she didn’t want the Guardia to find the key. She had €1.7 million in proceeds of crime stashed in that box back in Milan.

“Take the key”, instructed the lawyer, “and hide it in the chauffeur’s clothing.”

The lawyer then spoke to the chauffeur and told him to put the key in his underwear.

Anna Bettozzi with high boots, a python coat, snake boots (Source: Instagram)

Catch and Release

The officers listening in on the intercepted call then phoned the Guardia in Ventimiglia, who had detained Bettozzi, and told them that Bettozzi had told her lawyer about a lot of money hidden in a safety deposit box at the Gallia Hotel in Milan, and that the key was going to be stashed in the underwear of the chauffeur.

Law enforcement agencies will often conduct a controlled intervention where they cause a disruption to a suspect’s routine because it causes suspects to panic and react. Often the first thing suspects do is call the lawyers who helped them paper-up shell entities, and then they call their crime partners. They call those lawyers because they are concerned with the paper trail; they call crime partners because they are concerned with the money trail.

The Guardia decided to do a “catch and release,” and let Lady Oil continue her trip to the Cannes Film Festival after they seized the €300,000 in her boots.

When the safety deposit box was opened in Milan, law enforcement found €1.7 million in cash, wrapped up in baggies.

Money in baggies from Operation PetrolMafias (Source: Guardia di Finanza)

From May 2019 to April 2021, the police continued listening to Bettozzi’s phone calls and those of her lawyer, and learned how two powerful Mafia organizations – the Camorra and ‘Ndrangheta – helped turn her failed business around by buying illegal oil and gas from as far away as Kazakhstan and Russia, and importing it into Italy.

Early Life in Sardinia

Anna Bettozzi grew up on the island of Sardinia. She always had dreams of being famous. In a 1999 article in Italy’s La Repubblica, after her house had been robbed, she was quoted as saying that she “dreams of conquering the world”.

She went into real estate in the hopes of meeting one of the many Russian Oligarchs, other billionaires, actors and European royalty who summer on Sardinia’s Emerald Coast each year.

She came up with the stage name Ana Bettz, and pivoted to singing, self-financing several CD albums. She had a small following in Russia. In 1997, she paid for Michael Jackson’s producer to work on her first music video called “Ecstasy”, hoping it would give her career a boost. It didn’t.

Ana Bettz singing “You Are the One” (Source: YouTube)

She married a wealthy Italian oil dealer named Sergio Di Cesare, who controlled Europetroli SRL, an oil reselling business.

Di Cesare had a summer house in the Porto Rotondo area of Sardinia, beside Italy’s Prime Minister, Silvio Berlusconi. Bettozzi and Berlusconi became close friends. Very close.

Bunga Bunga Parties

During this time, the Italian Prime Minister was regularly hosting his now famous “bunga bunga” parties, which were after dinner sex parties for wealthy old men. At these “bunga bunga” parties, young women were hired to dress up in costumes, and perform sexual acts for Berlusconi and his old male guests. At least one girl regularly hired was underage – 17-year-old Karima el-Mahroug.

Bettozzi was also very close to Dario Lele Mora, one of the men who procured young women for the Prime Minister’s sex parties.

Berlusconi and Mora were both charged and convicted of prostitution-related charges. At Mora’s trial, el-Mahroug testified that “a singer close to Berlusconi attended the [bunga bunga] parties” – that singer was Bettozzi.

For at least six years – from 2006 to 2012 – Bettozzi hosted her own famous parties every August at her husband’s villa in Sardinia with Berlusconi.

Russian Oligarch Roman Abramovich, a close friend of Berlusconi, arrived in Sardinia for many of the Bettozzi-Berlusconi hosted summer parties, with numerous other wealthy Russian men on his superyacht “Le Grand Bleu.”

Russian President Vladimir Putin, not to be left out, went to Sardinia too, to hang out with Berlusconi in August. What did they do there? Only Bettozzi can say for sure.

Obstruction of Justice and Witness Poisoned

After his conviction, Berlusconi threw his wealth into one appeal after another and was eventually acquitted on appeal. But the case didn’t stop there. He was then accused of obstruction of justice for bribing witnesses, allegedly paying as much as €10 million to Karima el-Mahroug, who changed her testimony.

Another young witness died of a mysterious poisoning. If it was Novichok, the deadly nerve agent developed by Russian scientists to poison opponents of the Russian government, it would be undetected in an autopsy. Novichok was the nerve agent used in the attempted murder of Alexei Navalny.

The obstruction of justice proceedings against Berlusconi have been going on for 8 years. The prosecutor in the case alleges that Berlusconi’s “bunga bunga” parties involved sex slavery, and that Berlusconi gave away money, houses, cars and horses to stop witnesses from testifying against him.

Death of SergioDi Cesare

In 2018, Di Cesare died, leaving his oil business in shambles and with significant debt. Bettozzi took over the ailing business. Lele Mora was right there too, fresh from prison, helping Bettozzi at oil and gas shows.

Bettozzi needed capital to buy equipment, hire employees, operate the business and buy oil. She also needed petrol sellers and introductions to a network of buyers.

But no one in traditional finance would invest in a business operated by one of Berlusconi’s entertainers.

Using Facebook to find Mafia Associates

Using Facebook, Bettozzi reached out to Alberto Coppola, an associate of the Camorra in Naples. Coppola was known to be an expert in trade-based money laundering in the oil and gas sector, with expertise in fictitious invoicing.

Coppola agreed to help Bettozzi. He brokered deals for financing with three powerful Camorra Mafia families, the Moccia, the Formicola, and the Casalesi, which allowed Bettozzi to revive the fortunes of the company.

Disguising Fuel Imports

Coppolla helped to operate the business, while Camorra leader Alberto Moccia provided underground contacts to buy illegal oil and gas from Eastern Europe, and traffic it in Italy. One method they used was disguising diesel fuel as agricultural fuel in trucks outfitted with special levers that could add dye to fuel in tanks to change its color to fool inspectors.

Mafia accountants Claudio Abbondandolo and Maria Luisa Di Blasio oversaw payments of dirty money. The ‘Ndrangheta had to approve the deal with the Camorra and Bettozzi. The Camorra became the intermediaries between Bettozzi and the ‘Ndrangheta, who agreed to let the Camorra finance Bettozzi in exchange for a cut and for money laundering services.

Extortion Payments

Sales of the company grew to a whopping €370 million in 18 months – all of it dirty money. Bettozzi expanded beyond oil trafficking and joined the Mafia in forcing businesses to pay extorting payments under threats of violence – Russian Oligarch style, where extortion payments were filtered up to leaders in a pyramid scheme.

For several years, the DIA and Guardia di Finanza intercepted and recorded phone calls between Bettozzi, Coppolla, the Camorra and the ‘Ndrangheta.

Taking in over €8 Billion per Year

During one of those phone calls the police were intercepting, Bettozzi told her sister that she was working with the Camorra, and they were earning between €25 million to €30 million per day.

That’s €8.1 billion per year.

Although very secretive, the‘Ndrangheta went into business with Bettozzi because, as they were heard saying during an intercepted phone call,“trafficking oil yields more than trafficking drugs,” meaning it was more lucrative to traffic oil.

Kazak Oil

The police had recorded a meeting in ‘Ndrangheta-controlled territory in the town of Vibo Valentia. The meeting was between the Mafia and representatives of the Kazak oil company, KazMunayGaz, discussing oil sales to service Calabria.

The discussion involved the possibility of building a transshipment dock in the ocean to dock oil tankers, so that oil shipments could be delivered to Italy without passing through the Port of Gioia Tauro. They didn’t want it to transit through the Port of Gioia Tauro because it is controlled by other ‘Ndrangheta families who were not part of their money laundering business.

‘Ndrangheta Control

Although Bettozzi originally struck her deal with the Camorra, the ‘Ndrangheta – perhaps because of its greater power in the global organized crime hierarchy – dominated the financial side of the business and controlled most of the shell companies, properties and bank accounts used to launder the dirty money.

The Lady Oil’s Empire

Bettozzi boasted that she had “created an empire larger than Berlusconis”, and that she was so important, Berlusconi called her several times a day and she often did not take his calls. When she did talk to Berlusconi, the police heard those calls too.

In addition to a luxury apartment in Milan, Bettozzi had a sumptuous gold-infused villa in Rome’s upscale district of Appio-Pignatelli, with a blue lagoon pool, gold furniture, and rococo fireplaces, not far from the home of fashion designer Valentino.

Under her stage name Ana Bettz, she often Instragrammed herself in her villa, or posted photos of herself at the villa on Facebook, wearing high boots and tight clothes.

Anna Bettozzi in her villa instragramming about her Versace carpet (Source: Instagram)

Arrest and Sentencing of Bettozzi

The Guardia di Finanza and DIA decided to end “Operation PetrolMafias” on April 8, 2021, with the arrest of Bettozzi, her lawyer, Mafia leaders and 60 other people in several early morning raids across Italy and Europe.

Guardia di finanza: operazione PETROL MAFIE (Source: YouTube)

Bettozzi was charged with membership in an organized crime group, association with the Mafia, extortion, money laundering, and a host of other charges.

According to police, she arranged, through law firms, to make corporate changes of shell companies to keep members of the criminal association off the corporate records and obfuscated from investigations. The money they earned was used to buy luxury cars and real estate, and was laundered through 100 private companies and bank accounts associated with those companies in Hungary, Bulgaria, Greece, Malta, England and Croatia.

Over €360 million in cash was seized and over €1 billion in assets, including properties and companies.

Last week, Anna Bettozzi was sentenced to 13 years in prison, and Europe’s biggest dirty oil trafficking case came to a close. While police found €360 million in cash, there is still over €30 billion in cash missing.

Rise of the Petrol Mafias

The phenomena of Petrol Mafias is far from over in Europe.

As the ‘Ndrangheta said in intercepted phone calls, trafficking in stolen oil is more lucrative than drug trafficking. With the energy crisis, the opportunities for organized crime to make more profits from illegal petrol trafficking is exponentially greater.

Global energy frauds are coming fast and furious from all directions including at the retail level with pump fraud in Asia, at the pipeline level in Mexico from cartels that siphon oil directly from pipelines while it is in transit; and crude oil theft in Africa. Nigeria lost more than 115,000 barrels per day to oil theft over a 12 month period.

Climate change is key driver for military Arctic visibility

Climate change and Arctic

Last week, the US Department of Defense announced the establishment of new unit in the Pentagon, the “Arctic Strategy and Global Resilience Office,” situated in Alaska, to build preparedness to address climate change, and strategies to defend the Alaska Arctic-fronting coast.

After the Cold War, the US was occupied in other theatres; in particular, terrorism and the Middle East, and the Arctic region was not its military priority. It is now refocusing on its two peer competitors – China and Russia – and in the Arctic.

It makes sense – the convergence point of Russia, China and climate change is the Arctic circle.

There are only 8 Arctic countries – Russia, Canada, Denmark, US, Iceland, Norway, Sweden and Finland.

Arctic countries (Source: Britannica)

A number of factors are driving the US desire to have a renewed presence in the Arctic.

As a result of global warming, temperatures in the Arctic are rising three times as fast as the world average. The Arctic ice surface is shrinking by 1.6% annually, and now, 70% of the Arctic ice is seasonal. The reduction of the Arctic ice surface, and the seasonal nature of the ice means the Arctic Ocean is becoming more navigable for more days each year.

NASA Goddard (Source: YouTube)

Russia’s North Sea Route

That has opened up the Northeast Passage (also called the Northern Sea Route) which follows the Russian territory, and the Northwest Passage, which follows the Canadian territory and creates shipping lanes through the Arctic.

The Northeast Sea Route connects the Atlantic and the Pacific Oceans, is 40% shorter than the route through the Suez Canal and bypasses the Straits of Malacca and Hormuz, which are politically unstable.

Why Russia is Building an Arctic Silk Road (Source: YouTube)

As global warming becomes worse, shipping through the Northern Sea Route is expected to grow but such growth is not without geopolitical concerns; if shipping routes move to the Northeast Passage over the next few decades, it will shift power and wealth to Russia because the sea route is almost completely inside Russian territorial waters.

Canada’s Northwest Passage

Canada has the second largest land mass in the Arctic, and controls the Northwest Passage but unlike Russia, Canada has not developed or militarized its Arctic territory and some say Canada hasn’t taken Arctic sovereignty seriously. Sixteen years ago, Canada announced plans to build a naval refueling facility in Nanisivik – its only proposed military facility – but still hasn’t finished building it. For decades, legal scholars have said that because Canada does not defend, or take an interest in investing to defend, the Arctic, it may lose its Arctic footprint – likely to the US.

Russia’s Arctic military expansion

Russia has built significant settlements, infrastructure, ice-capable shipping ports, and three new military bases in the Arctic, including its large Northern fleet, and has expanded and modernized a dozen legacy military bases and airfields across the Arctic, including Rogachevo on Novaya Zemlya.

Russian Arctic instatllations (Source: Arctic Review on Law and Politics, August 2022)

Inside Russia’s Arctic Military Base (Source: BBC News YouTube)

The new bases, commonly referred to as “Arctic Trefoil” consist of one central living and administrative building in a triangular shape. There is one base in each of the western, central and eastern part of the Russian part of the Arctic.

China and Japan have Arctic ambitions

Meanwhile China and Japan, both non-Arctic nations, are building new transportation, infrastructure and commercial capabilities tied to the Arctic. In its 2021 five-year plan, China has said it will be involved in Arctic development. It is already launching a satellite for Arctic observation.

Both Japan and China are building nuclear-powered icebreakers to navigate the Arctic Ocean, ostensibly for “science.” Both are major investors in Russian LNG infrastructure projects in the Arctic off Siberia, and in LNG projects in Canada.

Access to resources

The Arctic is rich in rare earths and strategic minerals and contains vast oil and gas reserves. As the Arctic ice surface recedes, those resources will become accessible to Arctic nations for potential exploitation.

As climate change becomes more extreme and causes the loss of arable lands, and resultant human displacement, there will be renewed pressure on access to more basic Arctic resources – water and fish – from Arctic and non-Arctic nations, and the defence against IUU fishing in the Arctic will become more urgent.

The Chinese fishing fleet, which engages in the majority of IUU fishing around the world, is bigger than any navy in the world, and bigger than most navies combined.

By setting up the new Arctic Strategy and Global Resilience Office, the US military presence in the Alaskan Arctic will enable it to better understand how climate change will affect the international security environment and use that to inform military decisions.

More Arctic developments are likely to be announced within the next five years or sooner – for example, Canada may cede some sovereignty to the US and agree to the installation of a US military base on Canadian Arctic territory; and if that happens, Russia may follow suit and do the same with China.

New charges levied against Dhillon and against his lawyer

Three times a charm or a curse?

A Vancouver doctor who allegedly partnered with the now-infamous Vancouver lawyer Frederick Sharp in an international microcap alleged fraud scheme (summarized here) – Avtar Singh Dhillon – was charged criminally by the US Government, the FBI announced yesterday. It’s the third set of securities-related charges against Avtar Singh Dhillon in thirteen months.

Less than a week ago, Avtar Singh Dhillon (“Dhillon“) was charged by the Securities and Exchange Commission (“SEC“) for alleged fraud in connection with undisclosed promotional activities to sell the stock of Emerald Health Pharma Inc. (those charges are summarized here).

Yesterday, the FBI announced that Dhillon was charged with conspiracy in connection with payments to the same stock promotor of Emerald Health Pharma Inc. (“EmeraldPharma“).

In connection with another microcap company, Arch Therapeutics Inc., the FBI announced that Dhillon was charged with failing to disclose stock sales and with aiding and abetting the sale of unregistered securities.

Dhillon’s lawyer charged

Dhillon’s lawyer, Daniel V. Martinez, was charged with the sale of unregistered securities.

The FBI alleged that Martinez created a company for Dhillon and shares of Arch Therapeutics Inc. were parked there (meaning the lawyer created the central securities register and entered Arch Therapeutics Inc. as the shareholder of that private entity the lawyer incorporated in California). The private entity then sold the shares of the public company. Because it was a private company selling and fronted by the law firm, it looked to the outside world like it was not Dhillon beneficially controlling the shares. Dhillon earned US$1.3 million in proceeds of that crime. The securities disclosure of that issuer did not disclose these events to investors or to the capital markets.

Avtar Singh Dhillon, the former chair of the board of directors of the Massachusetts-based company Arch Therapeutics, and attorney Daniel V. Martinez have agreed to plead guilty to selling unregistered securities following an #FBI Boston investigation. https://t.co/lQEmuuBRI1

Both agreed to plead guilty. Dhillon is facing a term of incarceration of up to 30 years. No date has been set for Dhillon’s sentencing. He will be sentenced pursuant to US federal sentencing guidelines in effect as at the date of the events.

Because he was heavily lawyered-up in Vancouver throughout the whole of his capital markets career, including partnering during that career with a Vancouver securities lawyer, there isn’t much he can advance downwards for the sentencing guidelines. The 30 years is a baseline – it can be increased, for example, if a person directed the intimidation of a whistleblower, attempted to obstruct justice or refused to accept responsibility. There is usually a “role enhancement”, that increases sentencing where the person was in charge. Sentencing can also be reduced (called downward departures) if, for example, a person was young and made a mistake. A defendant who enters a guilty plea is not automatically entitled to an adjustment for acceptance of responsibility because it can be outweighed by conduct that is inconsistent with acceptance of responsibility such as a defendant telling family members or business partners that he’s going to get off. The SEC, in the Frederick Sharp case, alleges that several instances of the obstruction of justice emanated from Dhillon, including in connection with a purported land transfer.

Emerald Pharma and Sciences

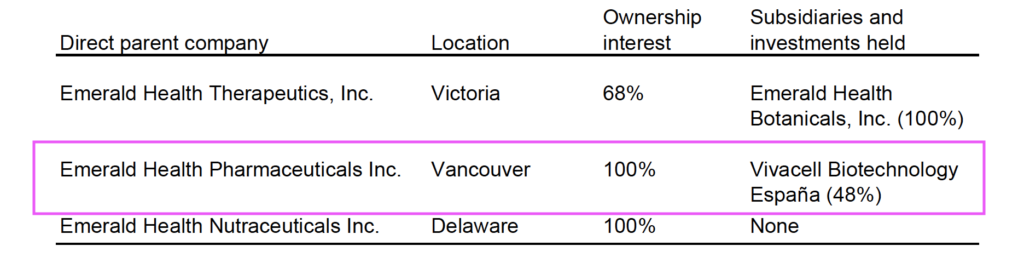

According to the Vancouver office of Deloitte LLP, and the last available consolidated financial statements they created of Emerald Health Sciences Inc., Emerald Pharma is owned 53% by Vancouver-based Emerald Health Sciences Inc., and it used to be a British Columbia entity that moved jurisdiction to Delaware.

In the charges announced last week, the SEC alleged that Dhillon caused officers of Emerald Pharma, whom he directed as a director, to draft fake consulting agreements to obfuscate payments to undisclosed stock promoters, and Emerald Pharma then paid fake invoices rendered by the promoters. Dhillon settled that case with the SEC and didn’t have to pay a fine for the alleged wrongful conduct. It is possible that he avoided civil penalties because of the then-undisclosed criminal charges announced today against him related to Emerald Pharma.

Dhillon voluntarily disclosed the list of shareholders of Emerald Health Sciences Inc. in a Court proceeding, and in that list Martinez appears as a shareholder.

Excel of stockholders of Sciences (Source: From Avtar Dhillon)

Dhillon was dealing with the death of his father-in-law the last few weeks, and it is likely that the FBI, US Department of Justice and SEC delayed making an announcement in respect of Emerald Pharma to allow him to deal with family matters.

Addinginternal controls

Emerald Pharma issued a news release two days ago (here) in which they stated that they intend to “add internal accounting controls.”

Wait – they’re going to “add” internal controls? Why were there no internal controls before?

Since Deloitte LLP completes (perhaps “completed” if they have resigned from Pharma and Sciences), the financials of both entities consolidated together, it begs two questions – how it was able to issue audited financials without internal accounting controls in place for a public company, and whether Deloitte LLP informed Emerald Health Sciences Inc. (as control person and pursuant to consolidated financials that included Emerald Pharma), that there was a significant deficiency in internal controls. An auditor is required to report on internal controls to the client and more importantly, to the capital markets.

If they didn’t, that’s an issue for Deloitte LLP; if they did, that’s an issue for Emerald Pharma.

Controversial entity

As noted here, Emerald Health Sciences Inc. is a controversial entity because Dhillon swore in an affidavit years after soliciting investments from investors, that one of its co-founders is Yadvinder Singh Dhillon. Singh-Dhillon is a US felon who was convicted of smuggling one of the largest amounts of heroin into the US with Ranjit Cheema, the deceased leader of an Indo-Canadian organized crime group. The Emerald Health Sciences Inc. entity controlled a number of public companies. One of those companies entered the legalized cannabis space in Canada and obtained a federal cannabis producer licence with the US felon in the mix.

How any of that was possible remains a mystery. Singh-Dhillon’s criminal history was well-known because the heroin smuggling case was heavily covered in the media for over a decade in Canada.

Dhillon incorporated a company in California through Martinez that they decided to name “Walk on Water” – an expression that means a person believes he or she is untouchable, superhuman, godlike. One suspects the FBI may have some views on that.

A Vancouver doctor who allegedly partnered with Vancouver lawyer Frederick Sharp in an International microcap fraud scheme (summarized here) – Avtar Singh Dhillon – was charged by the Securities and Exchange Commission (“SEC“) again today. This time it involves a different public company and hits closer to home for Vancouver residents because the company is Emerald Health Pharmaceuticals Inc. (“EmeraldPharma“).

Emerald Pharma is owned 53% by Vancouver-based Emerald Health Sciences Inc., according to Deloitte LLP’s Vancouver office, which completed consolidated financial statements of Emerald Health Sciences Inc. which included the financials of Emerald Pharma.

Emerald Pharma was incorporated in Delaware in 2017, but according to Deloitte LLP, before that it was a British Columbia company located and operating in Vancouver since May 2015, and was wholly-owned by Vancouver’s Emerald Health Sciences Inc.

Emerald Health Sciences Inc. is a controversial entity because it is the control person (in the US securities common law sense) of a number of public companies but was co-founded by a US felon who was involved in one of the largest heroin smuggling cases in US history. This was not disclosed to investors at the time, but was revealed years later in an affidavit Dhillon voluntarily filed in a Court proceeding, together with a list of all of the shareholders with their addresses of the Sciences entity (which included nominees that the SEC says are, or were, controlled by Frederick Sharp). The Ontario Securities Commission held, in the Russian gangster case involving the FBI’s most wanted, Simeon Mogilevich, that criminality must be disclosed to investors, as a matter of risk. How they found a solicitor willing to do securities work with a felon co-founder is a mystery.

Subsidiaries of Emerald Health Sciences Inc. Source: Deloitte LLP, 2016

The SEC also charged Emerald Pharma and its CEO James DeMesa (“DeMesa“).

Undisclosed stock promotions

The SEC alleges that Avtar Singh Dhillon (“Dhillon“) and DeMesa hired a newsletter writer to write purported independent articles to promote the stock of Emerald Pharma without disclosing that the articles were paid promotional content and without disclosing who received the payment (a §17(b) issue).

According to the SEC, several executives from Emerald Pharma (whom they do not name), attended a meeting in November 2019, to work on the promotional plan, subsequent to which the SEC alleges that Dhillon arranged to secretly pay the promoter to promote a Reg A offering to US investors.

The SEC alleges that Emerald Pharma entered into fake consulting agreements as a method to move money to pay the promoter secretly.

Fake consulting agreements

Vancouver capital markets has the dubious distinction of having invented the idea of fake consulting agreements to move money, which on its face is a form of trade-based money laundering (“TBML“). TBML revolves around invoice fraud for goods or services whereby goods or services are over or under-priced, or there are invoices for no goods or services. TBML can be domestic or across state or national lines. The SEC says that in this case, fake invoices were submitted to Emerald Pharma for payment with work described on the invoices as “developing agave syrup.”

The SEC alleges that it was Dhillon who urged DeMesa to enter into the fake consulting agreements on behalf of Emerald Pharma.

The SEC also alleges, without using these words, that the promoter was being paid as a finder, earning 6% of funds raised. Emerald Pharma paid the promoter US$1.7 million to promote, plus issued shares to the promoter with a value of US$600,000. Emerald Pharma raised USS$30 million from the alleged illegal promotions.

The SEC charged Emerald Pharma, Dhillon and DeMesa with numerous securities violations for their deception, allegedly employing various schemes to defraud investors, and making materially false statements in the disclosure material of Emerald Pharma.

The SEC sought injunctive relief against Emerald Pharma, Dhillon and DeMesa, and their attorneys among others, to prevent them from continuing to break the law. Why attorneys? Because attorneys are capital markets gate-keepers – they draft the continuous disclosure, and then publish the disclosure they write on Edgar or Sedar, which investors rely upon.

Parties settled

All of the parties charged settled.

Emerald Pharma agreed to pay a penalty – more like a parking ticket really, since they raised US$30 million – of US$517,955; DeMesa agreed to pay a penalty of US$103,591.

And Dhillon?

Although there are other securities fraud charges against him, including criminal charges in connection with other public companies, he got off Scot-Free. Not even $1 did he have to pay.

It’s hard to understand the logic, or the deterrent and denunciation message of a settlement with Dhillon on such terms. He was the director, e.g., the directing mind of the entity; the person living in the luxury mansion with the greatest capacity to pay (investors on the East coast told us that Dhillon flew around on a private jet with a body guard), who may prove to be a recidivist if the Frederick Sharp related charges are concluded with a conviction.

In a shareholder newsletter of the control person, Emerald Health Sciences Inc., DeMesa once said that his philosophy is to get outstanding business results by working closely as a team and by following the philosophy of Dhillon, which he said was to ” be a family and not just a typical business.”

But alas, they were no family – they booted DeMesa out of Emerald Pharma.

Hey, Be Happy!

DeMesa runs a YouTube channel on “being happy” with 5 subscribers.

Part 1 – Securities Fraud in Canada and l’affaire Uramin-Areva

Voyager Digital

“Asking Questions About Canadian Capital Markets” is a series of articles about the capital markets in which we explore some Canadian public companies and ask questions. These questions may shed light on the now-defunct Canadian digital currency exchange called Voyager Digital based in Vancouver.

One of the founders of Voyager Digital is a Canadian attorney named Stephen Dattels.

To understand Voyager Digital, we’re going to look at some of the public companies he was involved in before Voyager Digital.

Voyager Digital, the digital currency exchange, is a subsidiary of a British Columbia public company(1).

According to several media reports, some investors have filed a class action lawsuit in the US against Voyager Digital, alleging that it was a Ponzi scheme with US$5 billion allegedly missing(2).

When people talk about loses to investors, sometimes it’s not clear what they mean. In the case of digital currency exchanges, if they are public companies, there are two separate pools of investments – funds from investors who bought shares of the public company (e.g., shareholders), and funds from consumers taken in as a deposit-taking function and held in trust for consumers.

The billions of dollars allegedly missing according to the US class action lawsuit refers to the money that ordinary consumers deposited in trust to buy digital currencies, some of which are so-called “tokens” or so-called “stable coins” and most are a securities. This series of articles is not about that activity or consumers; it’s about the capital markets side.

In this Part 1, we explore historic attempts to federally legislate Canada’s capital markets and then we look at one of the public companies Dattels was at the helm of called Uramin Inc., which came to be know as the scandal “l’affaire Areva” or “l’affaire Uramin” in France.

Systemic securities fraud

There is a perception in Canada that legislators haven’t done much to address securities fraud in Canada. According to research we conducted in early 2021 (see Business in Vancouverhere), while Canada represents only 12.5% of the US population, it often represents 40% of securities fraudulent activities in the US capital markets involving micro-capitalized public companies. In 2020, we researched US Court records and calculated that there was over US$4.5 billion in open securities fraud cases involving Canadians in the US.

When Covid-19 fraud started occurring in the capital markets with false representations by microcap public companies stating that they had magic Covid-19 drugs or cures, the US Securities and Exchange Commission (“SEC”) issued emergency orders to stop misrepresentative statements by suspending the trading of securities on more Canadian public companies than companies from anywhere else in the world. The SEC v.Frederick Sharp et. al. alleged securities fraud prong of cases with British Columbia actors adds another US$1 billion to the tally of open securities fraud cases involving Canadians.

Canadian public companies cause more per capita harm to US investors and to the US capital markets than any other country. The schemes also involve American wealth stripping – e.g., removing wealth from the US to Canada, although it could also involve other countries. For example, the YBM Magnex case (see here) involved removing wealth from the US routed through Canada, destined for Russia. YBM Magnex Inc. is the first known case of state-sponsored securities fraud and wealth stripping in the capital markets but because of a lack of knowledge about Yvegeny Primakov in the West, the case was never viewed as one of state-sponsored activity.

The problem of securities fraud perpetrated by Canadians on American investors has been known to US lawmakers since at least the 1940s. In a New York Times article dated June 2, 1940, a reporter noted that the best suckers grow in the US, suckered by Canadian fraudsters who target the US investors because they want access to a wealthy, large investment pool they can’t get in Canada.

The Washington Post, in 1952, wrote that the US Senate’s concern for American investors being defrauded by Canadians with phoney stock claims, including phoney uranium mining claims, was so heightened that there was talk of a treaty just to ship fraudsters from Canada to the US where they could be prosecuted.

Fraud on the capital markets (called by its 1920s name, “public markets,” in the Criminal Code of Canada) is a predicate offence under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act, so if there is a capital markets fraud problem, we also have a money laundering problem in the capital markets.

From time to time, Canadian federal legislators have tried to address Canadian securities fraud and to force a cultural change using the law. Unfortunately, to no avail.

Bond Dealers Association of Canada

Canada was once ahead of its time in securities legislation discourse.

In 1916, the Bond Dealers Association of Canada was formed by a handful of nationally known bond house executives in Toronto – John Worth Mitchell of Dominion Securities Corporation Limited (now RBC Dominion Securities), J. H. Gundy of Wood, Gundy & Company Limited and A.E. Ames of A. E. Ames & Company Limited. They were famous financiers in Canada, the US and the UK who later ran (with E. B. Wood), Canada’s Victory Bond programs for the federal government for both World Wars.

In its first year, the Bond Dealers Association set up a committee at the request of the federal Minister of Finance to consult on securities matters.

In 1919, Bond Dealers Association leaders J.W. Mitchell, (who was previously an Ontario lawyer), J.H. Gundy and C.H. Burgess drafted a securities legislative framework which proposed that a federal securities commission be established in Ottawa, with branches in every province, to examine projects before securities could be sold to the public. Securities dealers would be required to be registered to sell securities and every issuer of securities for public sale would be required to provide full disclosure and any other information desired by the federal securities commission. The federal securities commission could reject a project that involved the issuance of securities to the public, and no offering of securities by advertising, circular or letter could be conducted without advance approval of the securities commission. The securities commission would be empowered to investigate issuers and their statements. Speculative securities would be “so marked on all literature.” The markings on securities literature would also include yield representations and any securities which promised to yield more than 7% return or that made representations to investors that the investment would be twice its value in two years, would have to be marked as speculative for investors. Those who violated the new proposed securities laws, could be fined or subject to imprisonment by the federal securities commission.

This was 14 years before the US Government enacted its federal securities laws and created the SEC. Canada did not enact federal securities legislation as proposed by a committee of the Bond Dealers Association but almost identical concepts were enacted in the United States in 1933 and 1934.

In 1921, the Bond Dealers engaged in discussions for Ontario’s proposed securities legislation. With the Toronto Stock Exchange, they were looking at investor protection legislation. A mining exchange called the Standard Exchange in Toronto pushed back, arguing that investor protection would harm the mining sector. The Globe and Mail noted at the time that the members of the Toronto Stock Exchange believed that mining companies on the Standard Exchange were of “questionable quality” and wanted protection for small investors, who they said had little opportunity to determine the merits of an offering.

For context, J.W. Mitchell, A.E. Ames and J.H. Gundy owned numerous utilities and financial businesses together in the United States and Canada, and sold bonds in New York. They were tight socially – for example, A.E. Ames hired the brother of J.W. Mitchell, who operated the London securities branch office of A.E. Ames & Company Limited. Dominion Securities Corporation Limited, was founded in 1901 and J.W. Mitchell, E.R. Wood, Sir Wiliam Mackenzie, and George A. Cox were among its founders and were officers or directors. Mitchell, Ames and Gundy were extremely well-connected to American industrialists and American bankers and often consulted American legislators on securities law matters with a view to ensuring that Canadian, US and UK securities laws were aligned to facilitate international finance during critical war and post-war periods.

Because they were in International finance and securities specifically, they were more acutely aware than most that harm to investors from securities fraud caused market distrust and would erode Canada’s ability to attract investment. While they had a personal interest in ensuring the market was operated with integrity, they also had a deeper obligation to Canada as the sellers of the federal bonds in international and national markets.

The way of the business world back then was through private clubs and for example, J.W. Mitchell for whom records survive, was one of a handful of Canadians invited to join the prestigious Bankers Club of New York and the Detroit Club frequented by presidents Truman, Hoover and Roosevelt. For all of their connections to federal lawmakers, access and power as the captains of bond finance in Canada, they were unable to bring about investor protection for securities on a national level in Canada.

But their legacy lives on – the Bond Association of Canada became the Investment Industry Regulatory Organization of Canada.

Bond Association of Canada founders J. W. Mitchell of Dominion Securities Corporation Limited (first from the left), J. H. Gundy of Wood, Gundy & Company Limited, A.E. Ames of A. E. Ames & Company Limited with E. B. Wood (third from the left), 1917 (Source: Collection of Sir Robert Borden).

Proposed federal securities legislation

In Canada in 2009, former Finance Minister Jim Flaherty set up a federal working group which drafted a federal securities act to replace provincial securities legislation. The legislation was designed to, among other things, address systemic fraud afflicting Canada’s capital markets, protect the Canadian financial system and investors, and enable the detection and prosecution of financial crimes arising from capital markets activities. Flaherty’s efforts were defeated by the Supreme Court of Canada which took a very provincial view and ruled in Reference re Securities Act, that capital markets had to remain provincial jurisdiction under The British North America Act, 1867.

The decision was rooted in a reality that existed in the last century when in Canada, capital markets were limited to Toronto and Montréal, and securities were evidenced on physical paper records and delivered to investors by horse and buggy.

The fact that the Canadian judiciary, in this day and age, thinks that the capital markets are like the 1890s is quite concerning.

Where Canada’s capital markets were born – King and Bay Street, Toronto, Canada, circa 1890 (Source: Toronto Public Archives)

Senate attempts to amend Criminal Code

In 2016, the second federal attempt was undertaken by former Canadian Senator Céline Hervieux-Payette, who was the deputy chair of the Standing Senate Committee on Banking, Trade and Commerce. She introduced criminal legislation called the “Combating International Fraud Act”, to respond to fraud in the capital markets after a number of scandals involving public companies in Canada left investors (many of whom were elderly) destitute and which harmed Canada’s financial reputation internationally.

Senator Céline Hervieux-Payette, 2017 (Source: Eric Carrière, Flickr here)

Senator Hervieux-Payette said she was motivated to introduce the legislation because of Stephen Dattels. Stephen Dattels appears to be the only Canadian attorney, perhaps the only attorney anywhere in the world, in respect of which deterrent legislation has been drafted.

Uramin Inc.

In Parliament, the Senator stated that Dattels founded a company in Canada called Uramin Inc., which became a public company in Canada listed on the TSXV. A short time after listing, Uramin’s stock price rose 467% and it was sold for €2.5 billion to Areva S.A., a state-owned nuclear energy corporation in France.

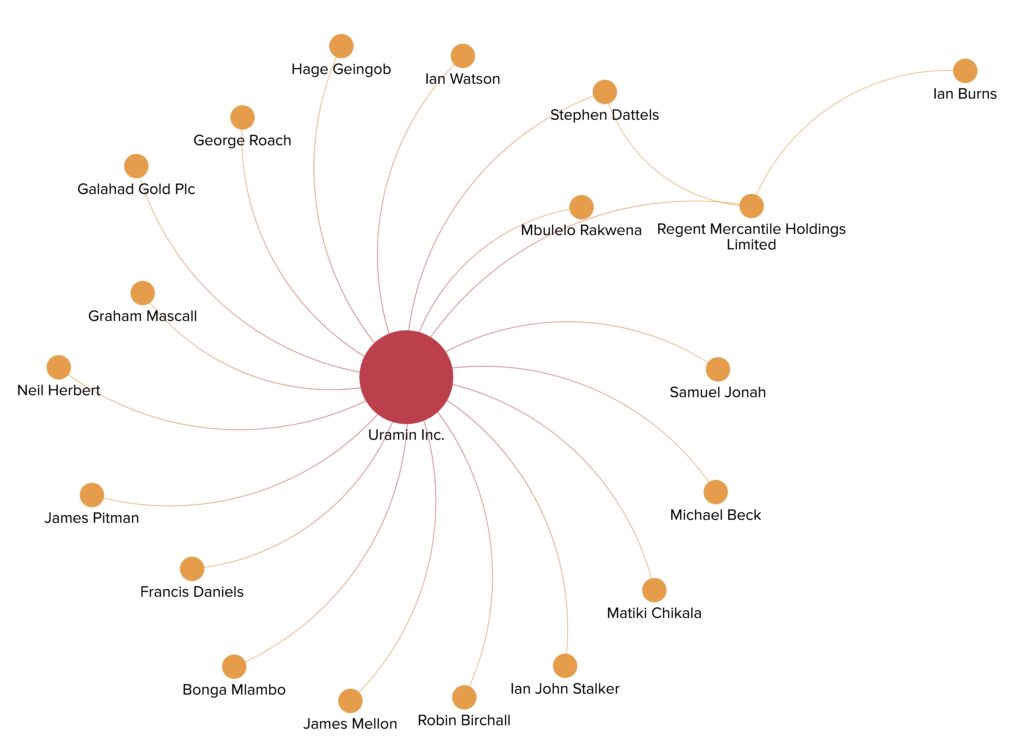

According to its filed securities disclosure and a book that Dattels had written about the deal, some of the people involved in Uramin Inc. with Dattels included John Ian Stalker, Samuel Jonah, Neil Herbert, James Pitman, Ian Watson, Graham Mascall, Michael Beck, Francis Daniels and the Brexiter James Mellon. According to a book they paid to be created about themselves and Uramin, the idea to start a uranium issuer stemmed from watching Frank Guistra and Ian Telfer start a uranium issuer with a Russian national.

A simple network of Uramin Inc. before it was acquired by Areva SA

Why did a foreign government pay €2.5 billion for a little public mining company in Canada that had only been around for 674 days, that had mined nothing? Investigators in France have theories but no one knows the answer. The CEO of Areva has testified before several federal bodies in France, and not all of her testimony has been made public. Part of the reason may be because of representations Uramin made about the extent or value of its uranium resources. Its disclosure says its uranium resources totalled 262.6 million pounds in three African countries.

The Senator told Canadian Parliament “there was no uranium” and she stated that various audits, including one by the French Parliament found that “Dattels and his associates lied outright about their uranium reserves and deposits.” We have not been able to find an audit document which confirms what the Senator stated.

No uranium? Some uranium?

In France it took a while for Areva S.A. management to comprehend its own uranium acquisition and it wasn’t until 2010, that it hired external investigators to find out about its own deal. What they and investigative journalists (see “Areva: les secrets dune faillite”here) say they learned was that: (a)Uramin Inc. had uranium deposits in Namibia that were not exploitable because they were below 100 ppm U (below 100 ppm is graded “very low” and means there is 0.01% U or less); (b) deposits at the Bakouma site in the Central African Republic were not exploitable because of mining land access issues; and (c) there were no uranium mining rights in South Africa (see “Affaire Areva Uramin: 3 milliards en fumée” here).

“Affaire Areva Uramin: 3 milliards en fumée” (Source: YouTube Channel of Imineo Documentaires)

Uramin’s mining report, called a 43-101, states that the Uramin deposits in Namibia were, for the most part, above 100 ppm U and were “low” and not “very low”. Low grade is 1,000 ppm U or 0.1% U.

With respect to the assets sold by Uramin in the Central African Republic, after the deal closed, Areva was unable to access the mining site it bought from Uramin, even though Uramin said it had paid US$27 million to the Central African Republic for a 90% interest in Bakouma and for licenses to commence mining activities.

Bakouma empty site

According to the Central African Republic, they were the shareholders of 10% of a Uramin subsidiary registered in the CAR which held the Bakouma mining rights, and its shareholder and mining agreement required the advance written consent of the CAR for the sale to Areva S.A., which was never given.

Areva negotiated with the President of CAR, François Bozizé, to re-acquire the mining rights it had already paid €2.5 billion for, and eventually agreed to pay another US$50 million to the CAR to access the mine site. The deal was negotiated by a New Zealand person, who acquired Belgium citizenship, but who lives in the Congo, named George Forrest. He is a controversial figure who, according to the US government, was talking to the Iranian regime about buying uranium. He attempted to do a capital markets deal for uranium in Canada, and was stopped by the US government. We’re going to look at George Forrest later in this series.

A person from Ghana named Samuel Jonah was the person at Uramin who dealt with President François Bozizé Yangouvonda‘s government to secure the mining rights.

Bozizé “opening up” the Bokouma empty mining site for Uramin in 2006

According to documents on Wikileaks, a bonus payment was allegedly also made by Uramin to officials in the CAR in June 2006.

Some in France have called the Uramin deal a scam (une escroquerie) or a fiasco (see “Affaire Areva Uramin: révélations due un scandal d’état?”here).

“Affaire Areva Uramin: révélations sur un scandale d’Etat?” (Source: YouTube Channel of CNEWS)

There were other aspects of “l’affaire Areva” that involved Canada beyond accusations about un-exploitable reserves, and those were concerns involving money laundering. And although they involved allegations tied to Uramin Inc., they don’t originate from Uramin.

Money laundered here and there?

The first is that, according to TracFin, the French federal financial intelligence unit, the spouse of the CEO of Areva, Olivier Fric, had access to material undisclosed information about Uramin Inc. and was able to buy securities of Uramin for several weeks during its blackout period. He conducted those securities transactions using a BVI shell company called Amlon Limited and netted €300,000.

TracFin told the French prosecutor that the transactions buying and selling the securities of the Canadian public company were suspicious transactions for money laundering purposes for fraud.

Spy thriller

One of the most interesting persons in l’affaire Areva was Saifee Durbar. He self-describes as a “bandit” and his role in l’affaire Uramin has been described in The Times as one of a key player in a spy thriller.

He told investigative journalists and the French government that millions of dollars in proceeds of corruption were paid to a South African named Tokyo Sexwale at the closing of the Uramin deal, which originated from ScotiaBank in Toronto. The funds, he alleged, were laundered to Bermuda and then to South Africa for the benefit of Sexwale. In 2017, he gave more specific statements in respect of Sexwale and Uramin (see “Candidat à la Fifa, Tokyo Sexwale, éclaboussé par une affaire de corruption” here).

L’OBS headline, February 16, 2016

Saifee Durbar was a whistleblower. He had information no one else did because he was an advisor to Bozizé with access to information about Uramin and its executives, and Areva and its executives, and their dealings with the CAR government both before Uramin acquired its mining license from CAR, and after, when Areva tried to access the mining site without an authorized change of control.

He twice told investigators that he is in fear for his life over l’Affaire Uramin. Why? What don’t we know that he does? We’re talking about a little Canadian mining issuer – who could he be afraid of?

The French national financial office established two inquiries to investigate Areva S.A., including aspects of the Uramin deal.

Side deal for corruption

At the end of the day, the prevailing theory among some people in Europe and Africa who were involved, and who spoke to investigative journalists, appears to be that the deal involved a side-deal where a portion of the acquisition price went into a black suitcase (see “Enquête Areva – Uramin, filouterie radioactive?” here). A black suitcase is an expression used in France and China, perhaps other places, that means a bag for black money. Black money is money for crime, most often to make corruption payments.

It was Areva’s black suitcase, though, not Uramin’s but the suitcase was in Canada, if it existed. And if it existed, when the suitcase needed to be opened, it was opened in Canada and the money it held was sent to intended recipients. By that I mean if foreign corruption payments were made, they were made from Canada. It can’t be otherwise because in any M&A deal, the deal proceeds are paid to one recipient in trust. That recipient then, on the authority of written consents to pay, disburses payments. Even if they disbursed to another black suitcase in the Bahamas, Bermuda or the Cayman Islands, it still came from Canada.

In France, “l’affaire Uramin” was a massive story for years. Several books have been written about it.

Senator Hervieux-Payette said that no securities regulator in any province conducted, or would conduct, an investigation into “l’affaire Uramin.” The Senator told Parliament that she tried to get the RCMP to investigate but that went nowhere, she said. Not even on the foreign corruption angle. The Senator then conducted her own investigation, which led to her proposed legislation to strengthen criminal enforcement of Canadian capital markets.

Her draft legislation included provisions for extraterritorial application of the Criminal Code insider trading and tipping offences. The latter provision, the Senator told Parliament, could have been used to investigate what she called the “Dattels gang.” She submitted her investigation report to Parliament.

But Parliament didn’t enact the Senator’s legislation. We asked a former investigator in France who investigated “l’affaire Uramin” for France, why there was no investigation in Canada if there was a case to be made, as alleged. He told us it was because Canada’s mining lobby group lobbied the Canadian government to take no action.

But how do we explain the fact that the Canadian media never picked up on or followed l’affaire Uramin even though it was so significant a story in France and Africa? The answer is language – most of the Areva and Uramin coverage, including about Dattels, is in French and from France and Africa.

It seems likely that the Uramin-Areva deal was about more than a black suitcase to help France make foreign corruption payments from Canada, where they could be assured there would be no investigation into foreign corruption, or from the capital markets side. It seems that something much more intense went on with the deal involving Africa, China, Russia and the nuclear energy industry as a whole. We’ll explore that later.

And Areva? 6,000 people lost their jobs in France, across the EU and across Africa, and the European nuclear energy industry was destroyed. Russia stepped in as the global nuclear energy leader.

And Canadian attorney Stephen Dattels? He moved to the United States, built a mansion in West Palm Beach, Florida, and kept a footprint in Ontario’s thoroughbred horse breeding country. But he also stayed involved in little Canadian public companies, including Voyager Digital.

We found him connected to a little Vancouver microcap company named BetterLife Pharma Inc., where he is mentioned in a fascinating lawsuit filed by a man named Aly Ismail, battling over a finder’s fee.

Next up

In Part 2, we continue our journey to understand Voyager Digital with a backwards look at what investigations in France have uncovered about l’affaire Uramin thus far.

In subsequent parts, we then take a look back at mining in Africa tied to Canada and Russia, and international spies in the mining industry. We then move forward and take a deep dive into hidden control persons, the suppression of warrant rights, and what Vancouver securities lawyers disclosed to investors in the disclosure record of another Vancouver issuer called BetterLife Pharma Inc., where Dattels appeared in a lawsuit over a finder’s fee, before ending to look at Voyager Digital.

Footnotes:

(1) There is sometimes confusion about jurisdiction in cases where a Canadian company decides to operate in other countries. A British Columbia company means its jurisdiction is British Columbia, and Canada. If it is a reporting issuer, the company makes a decision on which province it wishes to attorn to as a matter of jurisdiction for securities regulation and enforcement and in respect of investors. It also selects a principal regulator, and informs investors and securities regulators who that principal is. That provincial principal regulator has primary jurisdiction in Canada. A third prong in respect of jurisdiction is the jurisdiction of its directors. In the case of Voyager, it made the decision to report to all provinces and asked Ontario to be its principal regulator for investors. It has, perhaps had now, directors in Canada. That does not mean, however, that US securities and other regulators have no jurisdiction; they have jurisdiction in respect of US investors, financings and listing matters if a US exchange was used to list stock, and if securities were offered or sold to persons in the US.The US also has jurisdiction by virtue of correspondent banking rules, which means that all of the financial transactions of Voyager Digital fall under US jurisdiction, and that brings in the US Wire Act and financial crime laws.

(2) A Ponzi scheme simply means to take new investor money and use it to return money to old investors. Before Charles Ponzi, it was called “robbing Peter to pay Paul.” It’s one of the easiest alleged frauds to investigate and confirm because directors of a Ponzi scheme direct the making of statements about how much money is invested and held in trust and one call by a regulator to the DTC, or in the case of crypto, a review of its cold wallet holdings instantly affirms (or not) the truth of representations made to investors. That’s one of the things that happened with the Bernie Madoff Ponzi scheme – no regulator picked up the phone and called the DTC.

A mysterious man from Asia and the most famous round-tripping case

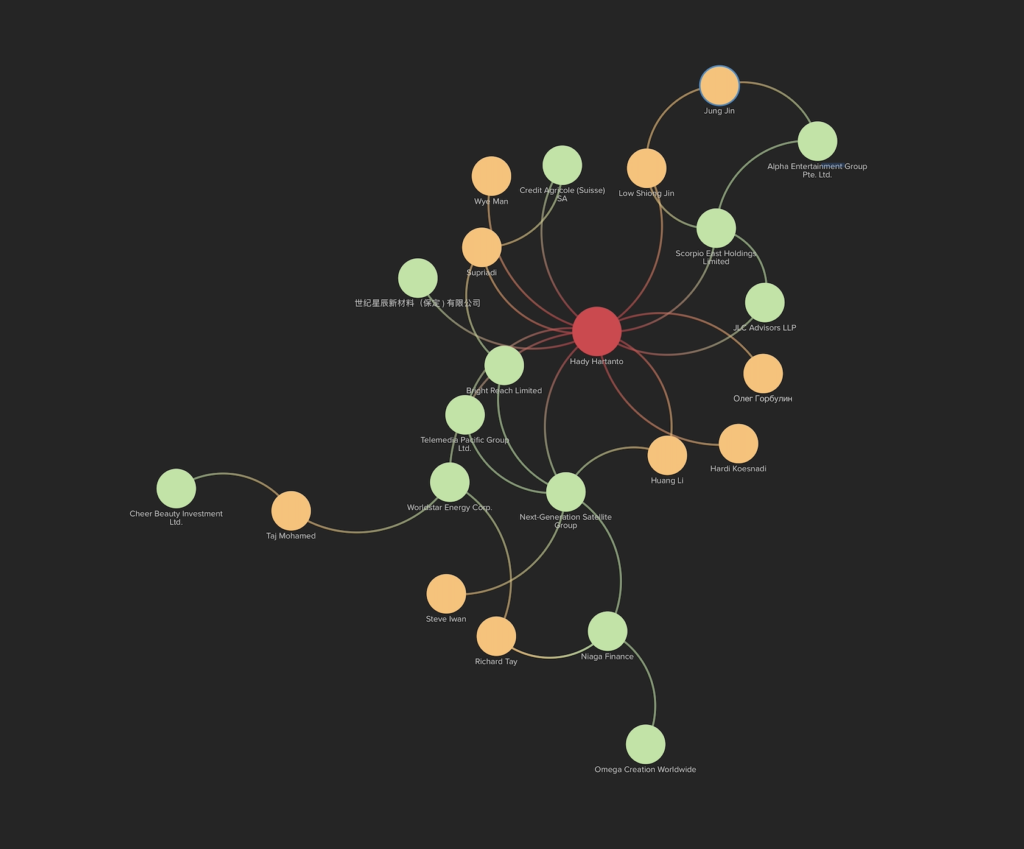

In Part 1 of “Understanding round-tripping in the capital markets” (here), we discussed round-tripping and looked at a rare SEC enforcement action involving round-tripping by executives of a microcap public company. In this Part 2, we look at the most famous round-tripping case involving a mysterious man from Asia named Hady Hartanto.

Hady Hartanto is a foreign national of Indonesia and China, and seems to have appeared in Vancouver, Canada, from time to time.

Early Vancouver-managed issuer

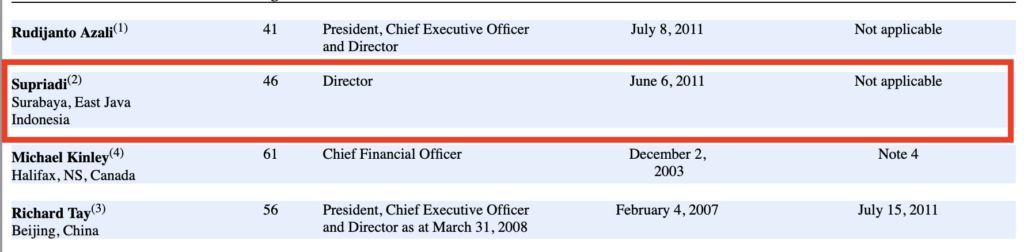

He has a long history of involvement in public companies in Asia but he also appears in an SEC revoked OTC-listed microcap company called Worldstar Energy Corp. managed from Vancouver. In 2007, Hartanto sold Worldstar 18% of 50 mining licences he said he owned in Mongolia, and thus became involved in Worldstar.

Worldstar Energy Corp. has one of the weirdest things in a US public reporting company – an anonymous person who was a director named “Supriadi”. No first name, no middle name, no last name – just “Supriadi”. That’s like appointing “Michael” as a director of a public company and hoping no one notices on the exchange, securities regulatory, corporate or AML banking side. Actually, no one did notice.

It is supposed to be against securities law disclosure rules to fail to identify a director of a pubic company.

When Hartanto became involved in Worldstar, Supriadi appeared too.

“Supraidi” in the Form 10-K of Worldstar Energy Corp.

One of the other directors at Worldstar with Supriadi was Richard Tay, a/k/a Tay Thai Seng, a Chinese national.

In Vancouver, Supriadi appears to have replaced a director named Taj Mohamed who controlled a British Columbia entity named Cheer Beauty Investment Ltd. Taj Mohamed was a “finder” and the control person of Worldstar, holding over 32% of its securities according to its filings.

Singapore Exchange action

The round-tripping case that is so famous started out as an enforcement action against Hady Hartanto and others by the Singapore Exchange in 2011 (see here).

The story goes like this – sometime in March 2011, Hartanto’s BVI company, Telemedia Pacific Group Ltd. (“Telemedia Pacific”), bought over 25% of the shares of a public company in Singapore named Scorpio East Holdings Ltd. (“Scorpio East“). Hartanto was appointed a director and officer of Scorpio East.

At that time, Scorpio East’s only potential business was film production revenues with several film producers who had signed on to create content worth S$12 million (the “Scorpio Contracts”). Scorpio East had paid a deposit of S$5 million for the Scorpio Contracts, representing 70% of its net asset value.